Our 6-Step Process

Step 1: Financial Foundations & Discovery

Outcome: Clear understanding of your current financial position

Experience a structured onboarding designed to make your initial steps easy and thorough. We'll begin by completing a comprehensive questionnaire, analyzing relevant documents, and understand your current or future cash flow needs to identify the important details of where you initially stand.

Establish your personalized eMoney financial planning dashboard, meticulously compiling key financial details including income, expenses, assets, liabilities, insurance policies, and estate documents. This step allows you to have a clear and simplified digital overview of your financial life, saving you time and energy moving forward.

Build the foundational layer of our custom Financial Planning Pyramid: focused on protecting against the "what-if" scenarios critical to an individuals or family's financial security. This includes identifying unexpected risks that may impact what you earn, what you own, what you owe, and those you love.

Step 2: Vision Mapping & Multigenerational Goal Clarity

Outcome: Define your personalized vision for a Brighter Financial Future™

Collaboratively identify and align your family’s financial priorities and objectives through thoughtful and meaningful conversations.

Clearly articulate and document personal and family goals such as retirement timelines, education and wedding planning, multigenerational support, philanthropic desires, and legacy intentions.

Transform your aspirations into tangible, achievable financial targets that provide you and your family with clarity, motivation, and direction.

Step 3: Strategic Analysis & Tax-Efficient Planning Strategies

Outcome: Identify strengths, gaps, and smarter paths to your goals

Conduct a thorough and insightful analysis of your existing financial strategies, identifying strengths, potential gaps, and opportunities for enhancement in investment portfolios, insurance coverage, and tax strategies.

Leverage our proprietary educational tools, such as the Three Tax Buckets, Insurance Types Chart, and Federal Tax Guides. We will also utilize eMoney’s Decision Center to illustrate the positive or negative impact of different strategies, and how small adjustments may have significant long-term value.

Develop customized, data-driven strategies aimed at maximizing tax efficiency, optimizing risk management, and accelerating your path toward achieving your defined financial goals.

Step 4: Brighter Future Blueprint™ Presentation

Outcome: Receive your clear, visual, actionable roadmap

Experience a personalized and engaging presentation of your Brighter Future Blueprint™, delivered digitally and in PDF format, clearly outlining actionable strategies, timelines, and progress indicators on your Financial Planning Pyramid.

Facilitate inclusive family sessions designed to bridge generational financial understanding, ensuring alignment and harmony with those who matter most to you.

Empower your decision-making with visual clarity and confidence, providing you with actionable insights and clear next steps.

Step 5: Implementation & Professional Coordination

Outcome: Efficient execution and seamless coordination

When you choose us to implement your financial plan, you will receive dedicated, hands-on support as we execute each aspect of your financial plan, from opening and funding accounts to reallocating investments, coordinating insurance needs, and updating beneficiaries.

Enjoy seamless professional coordination with your existing advisors—including CPAs, attorneys, realtors, mortgage consultants, insurance agents, and HR teams—or introductions to our vetted network of trusted professionals.

Experience clear communication, proactive updates, and meticulous follow-through, ensuring your plan is executed smoothly and efficiently, allowing you to remain focused on enjoying your life and doing what you do best.

Step 6: Monitoring, Adjustments & Generational Support

Outcome: Ongoing alignment and adaptability to life's changes

Benefit from regular, proactive plan reviews and real-time updates to your eMoney dashboard, ensuring your financial strategies remain optimized and relevant to market changes, legislative updates, and evolving personal circumstances.

Receive comprehensive annual support, including detailed cash flow management, mid-year tax strategy sessions, estate plan clarity, investment reviews, and insurance evaluations. Providing sustained clarity and confidence throughout your financial journey.

Gain continuous guidance and dedicated support through major life transitions—including college funding, job transitions, real estate transactions, selling a business, retirement, family caregiving, weddings, legacy planning, and managing inheritances—ensuring you and your family can thrive in every season of life.

The Brighter Future Blueprint™ is more than a financial plan—it's a structured, CFP® aligned process designed to organize your finances, grow your wealth, reduce taxes, and protect your family. Supported by advanced planning tools, professional coordination, and educational resources, we help you achieve clarity today and confidence about your future.

Let’s begin building your Brighter Financial Future™ today.

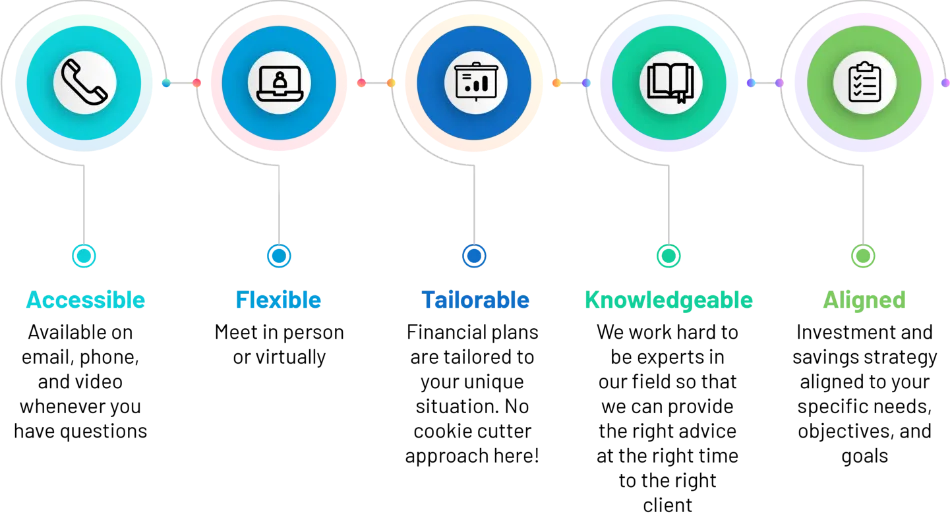

Comprehensive Planning

Built Around You

Our role is to simplify complexity, act in your best interest in our investment advisory services, and create a strategy that empowers confident decisions for you and your family.

These are the primary topics and questions that shape your financial plan and lead to better decisions as we work together.

Goal Creation & Values

Spending vs. Savings

Debt Management

Housing & Real Estate Decisions

Retirement Planning

Investment Strategies

Insurance & Risk Management

Tax Planning Strategies

Estate Planning

Education Planning

Small Business Owner Planning

This Process Helps You Become:

More confident

You will understand your financial life clearly and make decisions with greater certainty instead of doubt.

More strategic

Your wealth can grow with intention and better support your long-term goals.

More organized

We bring structure to your accounts, investments, and planning so everything is connected and efficient.

More protected

Your family, income, and future can be shielded from unnecessary risk.

More tax-efficient

You will keep more of what you earn by using smart strategies that match your situation.

More in control

You will know exactly where you stand, what is working, and what needs attention.

More aligned with your values

Your money will support the life you want to build instead of creating stress or confusion.

More at peace

You will feel more secure knowing your plan is monitored, updated, and moving in the right direction.

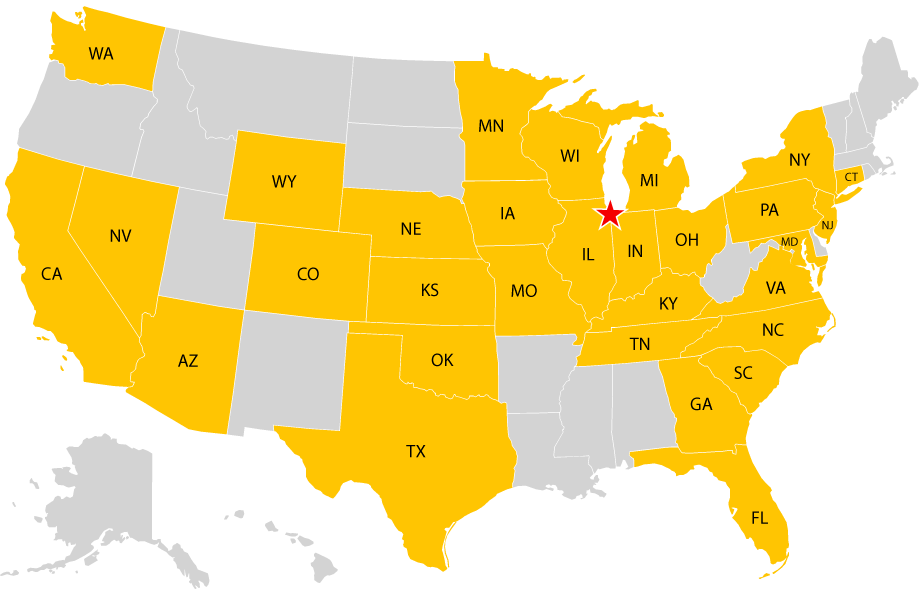

Our Location

475 North Martingale Road

Suite 1250

Schaumburg, IL 60173

Where We Do Business