Investments & Wealth Management

Eagle Strategies LLC is a Registered Investment Adviser and an indirect, wholly owned subsidiary of New York Life, and is a provider of holistic investment advisory and financial planning services. Our financial advisors leverage Eagle’s sophisticated wealth management platform, comprised of many of today’s leading investment managers, to design customized investment solutions to help address our clients’ unique investment objectives and risk tolerance levels. The breadth and investment knowledge of our Financial Advisors, coupled with Eagle’s diverse team of investment experts, allows them to provide the continuous financial guidance needed to help clients achieve long-term financial success.

Investment Advisory

Managing your wealth requires a clear understanding of your overall investment objectives. Eagle's comprehensive investment advisory capabilities utilize a disciplined investment approach that looks beyond traditional asset allocation, while addressing important factors such as risk tolerance levels and investment time horizons, to provide a clearer picture of our clients’ overall wealth.

Financial Planning

A comprehensive financial analysis of assets, liabilities, cash flow, and investments helps us identify a clear path to our clients’ prosperous futures. We’ll craft a detailed financial plan that helps you have the right wealth accumulation and preservation strategy in place to achieve your long-term investment objectives. More importantly, we continuously monitor and adjust our clients’ financial plans to ensure that they remain aligned with their stated objectives.

Investment Advisory Services Offerings

Fund Advisory Program

This program combines the expertise of professional third party investment managers with the personalized service and guidance of the Financial Advisor. By analyzing your overall investment goals, risk tolerance levels, and liquidity needs, we’ll help you determine which investment portfolio allocation, consisting of an optimal blend of nonproprietary mutual funds and/or exchange-traded funds (ETFs) is most appropriate for your investment goals and specific situation.

Separately Managed Accounts

Separately Managed Accounts (“SMAs”) are a type of professionally managed investment account that invest in individual securities on a discretionary basis and provide clients with the flexibility of restricting the holding of certain securities and tactically utilizing gains and losses for tax planning purposes. We will leverage Eagle’s robust offering of nonproprietary SMA strategies available through third-party money managers to either custom design a holistic investment portfolio or utilize individual strategies to address your specific allocation needs.

Rep Directed Program

This is an investment advisory program through which we will construct a customized portfolio of individual mutual funds, exchange traded funds (ETFs), and in some cases, individual securities, using the strategic asset allocation framework developed by Eagle Strategies and a leading institutional asset manager, or simply by us for you to review and approve. We’ll seek to utilize an optimal blend of asset classes that helps maximize long-term returns, manage overall portfolio volatility and achieve investment objectives while remaining aligned with your risk profile.

Investing isn’t just about choosing funds or reacting to markets — it’s about building a strategy that stays aligned with your life, goals, and long-term vision. At Sunny Financial Strategies, we combine disciplined planning, cost-efficient strategies, and modern technology to help you grow, protect, and manage wealth with clarity and confidence.

Our approach is simple:

No perfect investment. No perfect product.

But there is perfect planning — an investment strategy built around you.

All investment advisory services are offered through Eagle Strategies LLC, a registered investment adviser. All investments involve risk, including the potential loss of principal.

Our Investment Philosophy

We follow a long-term, research-driven approach enhanced by innovation and thoughtful creativity.

Most portfolios begin with strong fundamentals:

Broad diversification

Cost-efficient index strategies

Strategic asset allocation

Risk awareness tailored to your timeline

Tax-efficient structures

Modern planning and monitoring tools

At the same time, we think beyond the traditional.

For clients who want additional diversification, we evaluate well-designed alternative investments, private strategies, structured products, and principal-protected solutions when they appropriately support the broader plan.

Above all, our role is to bring organization, clarity, and discipline to your investment life — not to overwhelm you with options or push a certain product. Every recommendation is centered around what aligns with your goals.

How Our Investment Process Works

Your portfolio is built through our structured Brighter Future Blueprint™ process:

1. Understand Your Goals

We begin by learning your priorities, your comfort with risk, and where you are in your financial journey.

2. Organize Your Financial Picture

We review your accounts, pensions, retirement assets, liquidity needs, and tax considerations to understand the complete landscape.

3. Design Your Investment Strategy

We build a tailored portfolio using research-driven strategies, modern tools, and solutions that fit your long-term vision.

4. Implement With Clarity

You’ll know exactly how your portfolio works and why each piece is included.

5. Monitor, Adjust, and Improve

Your life evolves. Markets change. We continuously refine your strategy to keep everything aligned and forward-looking.

Types of Investment Accounts We Use

A strong plan uses the right account structure for the right goals. We help you understand and select the mix that makes sense for you.

Investment Advisory Accounts

(Professionally Managed Portfolios)

Investment advisory accounts give you access to institutional-level management, diversified portfolios, and strategies tailored to your goals, timeline, and preferences. These accounts are professionally managed, monitored, and rebalanced based on research-driven models and modern risk tools.

What this includes:

Broadly diversified portfolios built with ETFs, mutual funds, or individual equities

Aggressive growth, enhanced income, balanced, and custom portfolio options

Automatic rebalancing and continuous monitoring

Multi-asset strategies for risk management

Optional tax-aware or values-based portfolio designs

Broadly diversified portfolios built with ETFs, mutual funds, or individual equities

Aggressive growth, enhanced income, balanced, and custom portfolio options

Automatic rebalancing and continuous monitoring

Multi-asset strategies for risk management

Optional tax-aware or values-based portfolio designs

These accounts are ideal for clients who want long-term discipline, professional oversight, and an investment strategy that stays fully aligned with the broader financial plan.

Investment Advisory Services Offerings

Fund Advisory Program

This program combines the expertise of professional third party investment managers with the personalized service and guidance of the Financial Advisor. By analyzing your overall investment goals, risk tolerance levels, and liquidity needs, we’ll help you determine which investment portfolio allocation, consisting of an optimal blend of nonproprietary mutual funds and/or exchange-traded funds (ETFs) is most appropriate for your investment goals and specific situation.

Separately Managed Accounts (SMA)

Separately Managed Accounts (“SMAs”) are a type of professionally managed investment account that invest in individual securities on a discretionary basis and provide clients with the flexibility of restricting the holding of certain securities and tactically utilizing gains and losses for tax planning purposes. We will leverage Eagle’s robust offering of nonproprietary SMA strategies available through third-party money managers to either custom design a holistic investment portfolio or utilize individual strategies to address your specific allocation needs.

Advisor Directed Unified Managed Accounts (UMA)

This is an investment advisory program through which we will construct a customized portfolio of mutual funds, exchange traded funds (ETFs), and individual securities through SMAs, using the strategic asset allocation framework developed by Eagle Strategies and a leading institutional asset manager, or simply by us for you to review and approve. We’ll seek to utilize an optimal blend of asset classes that helps maximize long-term returns, manage overall portfolio volatility and achieve investment objectives while remaining aligned with your risk profile.

Brokerage Accounts

(Self-Directed, Advisor-Guided)

A brokerage account offers flexibility and control while still benefiting from professional guidance and thoughtful planning. These accounts give you freedom to invest across a wide range of options based on your goals, timeline, tax situation, and risk tolerance.

What you can invest in:

ETFs and index funds

Mutual funds

Individual stocks

Individual bonds

Certificates of Deposit (CDs)

Options

Why clients use them:

Building wealth outside of retirement accounts or can be used as a start-up retirement account without account minimums

Early retirement planning

Short-, medium-, and long-term goal funding

Liquidity and flexibility. No investment advisory fees.

Tax-loss harvesting and smart asset location

Brokerage accounts work well when you want transparency and flexibility combined with a structured, advisor-guided strategy.

Hybrid Investments with Principal Protection

(Investment Annuities)

Hybrid solutions—such as deferred investment annuities, could have both market-based and principal-protected features. These accounts are designed for clients who want growth potential with risk control.

They blend subaccounts that are similar to professionally managed mutual funds, fixed principal allocations that are linked to the underlying performance of a well-known index (ex: S&P 500 or Russell 2000), and fixed interest allocations- potentially all in the same account, or within different account structures.

Key benefits include:

Ability to participate in market growth

Guardrails during volatile markets that reduce risk

1Guaranteed death benefit to a beneficiary that protects at least the initial principal (minus withdrawals) or growth, whichever is higher

Options for future income or structured retirement planning

Potential for higher returns than traditional fixed assets like bonds, money market funds, or CDs

These accounts are often used to reduce downside risk, stabilize retirement portfolios, and complement long-term investment strategies. They’re not for everyone (usually ages 55+), but when used intentionally and in alignment with your plan, they offer meaningful protection and flexibility.

1All financial product guarantees are backed by the claims-paying ability of the issuer.

Three types of annuities to help you balance growth and security:

Fixed Deferred Annuities

A fixed deferred annuity offers steady savings growth with minimal exposure to market fluctuations. It’s designed for clients who prefer low-risk accumulation and want reliable outcomes.

What it offers?

A guaranteed interest rate for a set period — your money grows at a predictable rate.

Tax-deferred growth — earnings accumulate without immediate income tax until withdrawal.

No direct market risk — your principal is shielded from stock market volatility.

Customization — you can choose the contract term, access features, and beneficiary provisions.

Who it’s for?

Clients looking for long-term, conservative retirement savings who are willing to trade some growth potential for stability and predictability.

Important considerations

Although principal and earnings are protected from market downturns, returns are typically lower than growth-oriented investments. Early withdrawals may involve surrender charges, income taxes, and potential penalties.

Learn more about Fixed Deferred Annuities, offered by New York Life.

Variable Annuities

1Variable annuities offer access to investment markets with professional management and insurance features — suited for clients seeking growth potential alongside tax-deferred accumulation.

What it offers?

Market-based investment options via sub-accounts managed by professionals.

Tax-deferred growth until withdrawal — allowing your savings to compound without immediate income tax.

2Optional riders like accumulation benefit guarantees to protect portions of your investment under specific conditions.

Who it’s for?

Clients with a longer time horizon, comfort with market fluctuations, and the desire to integrate growth-focused investments within their retirement strategy.

Important considerations

Unlike fixed contracts, the value fluctuates with market performance. Variable annuities involve higher fees, surrender periods, and complexity. Withdrawals before age 59½ may incur penalties and taxes.

Learn more about Variable Annuities, offered by New York Life.

1 Investors are asked to consider the investment objectives, risks, charges, and expenses of the investment carefully before investing. Both the product prospectus and the underlying fund prospectuses contain this and other information about the product and underlying investment options and can be obtained from your Registered Representative. Please read the prospectuses carefully before investing.

2 Certain New York Life variable annuities provide access to an accumulation benefit rider called the Investment Preservation Rider 4.0 (IPR) which guarantees all premium payments from a loss that are made in the first policy year (less any proportional withdrawals) after the completion of a holding period. The rider is available for an additional charge. The IPR provides principal protection but does not protect the owner’s investment from day-to-day market fluctuations or against losses that could be realized prior to completion of the holding period.

Hybrid Variable/Index-Linked Annuities

1Hybrid annuities combine features of fixed/index-linked accounts and variable investment options, offering a flexible, blended strategy of protection and growth.

What it offers?

Fixed or index-linked components that guarantee your principal won’t fall below the original investment (under certain terms).

Variable component exposure, providing potential for market growth if you choose.

Tax-deferred growth with ability to transfer between account types inside the contract without immediate taxes.

Custom allocation between fixed/index-linked and variable portions based on your risk preferences and timeline.

Who it’s for?

Clients who want a “best-of-both-worlds” solution: some principal protection, plus participation in investment growth — suitable for those balancing risk and opportunity in their retirement planning.

Important considerations

The variable portion has market risk. The fixed/index-linked side limits downside but also may cap upside. Like all annuities, there are fees, surrender terms, and tax considerations.

Learn More about IndexFlex Variable Annuity, offered by New York Life.

1Variable annuities are long-term financial products used for retirement savings. There are fees, expenses, limitations and risks associated with this policy. All guarantees, relating to the variable account value, including death benefit payments, are dependent on the claimspaying ability of NYLIAC and do not apply to the investment performance or safety of the underlying Investment Divisions, as they are subject to market risks and will fluctuate in value. Index-linked account and fixed account guarantees are dependent on the claims-paying ability of NYLIAC. Withdrawals may be subject to ordinary income taxes and if made prior to age 59ó may be subject to a 10% IRS penalty tax. For costs and complete details, contact an agent. Please consider the charges, risks, expenses, and investment objectives carefully before purchasing a variable annuity. The product and fund prospectuses contain this and other information and can be obtained from an agent. Read the prospectuses carefully before you invest or send money. The New York Life IndexFlex Variable Annuity is issued by New York Life Insurance and Annuity Corporation (NYLIAC), a Delaware Corporation, and is offered through NYLIFE Securities LLC, Member FINRA /SIPC. Both NYLIAC and NYLIFE Securities LLC are whollyowned subsidiaries of New York Life Insurance Company, 51 Madison Avenue, New York, NY 10010.

Alternative Investments Accounts

(Private Market Investments)

Alternative investments are specialized, professionally managed strategies designed to complement traditional portfolios of stocks and bonds. These solutions provide access to asset classes typically available only to large institutions or sophisticated investors — and they are offered through NYLIFE Securities and Eagle Strategies for clients who qualify.

Who they're for:

Alternative investments are available only to Accredited Investors, Qualified Clients, or Qualified Purchasers, depending on the fund’s requirements. They’re intended for investors with a long-term horizon, a high tolerance for risk, and sufficient liquidity outside these positions.

Why Clients Consider Alternatives

Alternative investment accounts can support portfolios by offering:

• Broader diversification beyond stocks and bonds

• Low correlation to traditional markets

• Potential for enhanced income (especially private credit)

• Access to institutional strategies previously unavailable to individual investors

• Inflation protection (real estate, real assets)

• Potential for long-term capital appreciation (private equity)

These strategies are not meant to replace traditional portfolios — they’re designed to complement them when appropriate.

Important Considerations

Alternative investments also come with meaningful trade-offs:

• Higher risks and complexity

• Less liquidity (sometimes illiquid for long periods)

• Higher volatility in certain strategies

• More complex tax reporting (K-1 / K-3 in many cases)

• Higher minimums ($10,000–$50,000 depending on strategy)

• Not suitable for all investors

Compared to other investments we offer, alternative investments involve higher risk, are speculative, and are not suitable for all clients. They are intended for sophisticated investors able to bear high economic risks.

What’s Included Under Alternative Investments:

Private Credit

Debt-based investments not traded on public markets, including senior secured loans, floating-rate credit, direct lending, mezzanine financing, and distressed debt.

Why clients use it:

• Attractive yields compared to traditional fixed income

• Lower correlation to public markets

• Focus on income generation

• Potential resilience in different market cycles

Private Equity

Investments in privately held companies (startups to large private firms) through buyouts, venture capital, or secondary strategies.

Why clients use it:

• Potential for long-term capital appreciation

• Broad diversification into private markets

• Access to institutional-quality portfolios

Hedge Funds

Pooled investment vehicles using long/short equity, macro, quantitative, or event-driven strategies.

Why clients use it:

• Seek risk-adjusted returns with low correlation

• Potential for positive performance across varying market environments

Real Estate (Non-Traded REITs)

Institutional real estate portfolios including commercial properties, industrial assets, rental housing, data centers, and long-term net leases.

Why clients use it:

• Current income

• Potential for long-term appreciation

• Diversification

Real Assets

Investments tied to physical or infrastructure assets such as commodities, natural resources, equipment, land, and private infrastructure.

Why clients use it:

• Protection against inflation

• Low correlation to traditional markets

• Income potential in certain structures

Retirement vs. Non-Retirement Investing

Different account types serve different purposes, and we help integrate all of them into one unified strategy.

Retirement Accounts

401(k), 403(b), 457

Traditional & Roth IRAs

SEP IRA / SIMPLE IRA

Solo 401(k)s

Defined Benefit Plans

Our focus: tax efficiency, distribution planning, long-term stability, and ensuring your money supports decades of retirement income.

Non-Retirement Accounts

Taxable brokerage accounts

Trust accounts

Joint/individual investment accounts

Our focus: liquidity, tax-smart growth, income flexibility, and planning for short, medium, and long-term goals.

Why Clients Trust Us with Their Investments

Planning-first mindset — Your goals guide every decision.

Modern technology — Real-time dashboards, organized reporting, and ongoing insight.

Risk-aware approach — Thoughtful frameworks designed around your comfort level and timeline.

No sales pressure — We never lead with a product; we lead with your plan.

Complete coordination — Investments, taxes, insurance, and estate planning all work together seamlessly.

Forward-thinking creativity — Strategies that adapt to life changes, markets, and modern opportunities.

Because when everything is aligned, you’re able to move confidently toward the future you want.

Ready to Build a Smarter Investment Strategy?

Let’s review your current portfolio, identify opportunities, and build a strategy that matches your goals.

Investment advisory services are offered through Eagle Strategies LLC, a registered investment adviser. Eagle Strategies LLC is a Registered Investment Adviser and an indirect, wholly owned subsidiary of New York Life, and is a provider of holistic investment advisory and financial planning services. Our financial advisors leverage Eagle’s sophisticated wealth management platform, comprised of many of today’s leading investment managers, to design customized investment solutions to help address our clients’ unique investment objectives and risk tolerance levels. The breadth and investment knowledge of our Financial Advisors, coupled with Eagle’s diverse team of investment experts, allows them to provide the continuous financial guidance needed to help clients achieve long-term financial success. All investments involve risk, including the potential loss of principal.

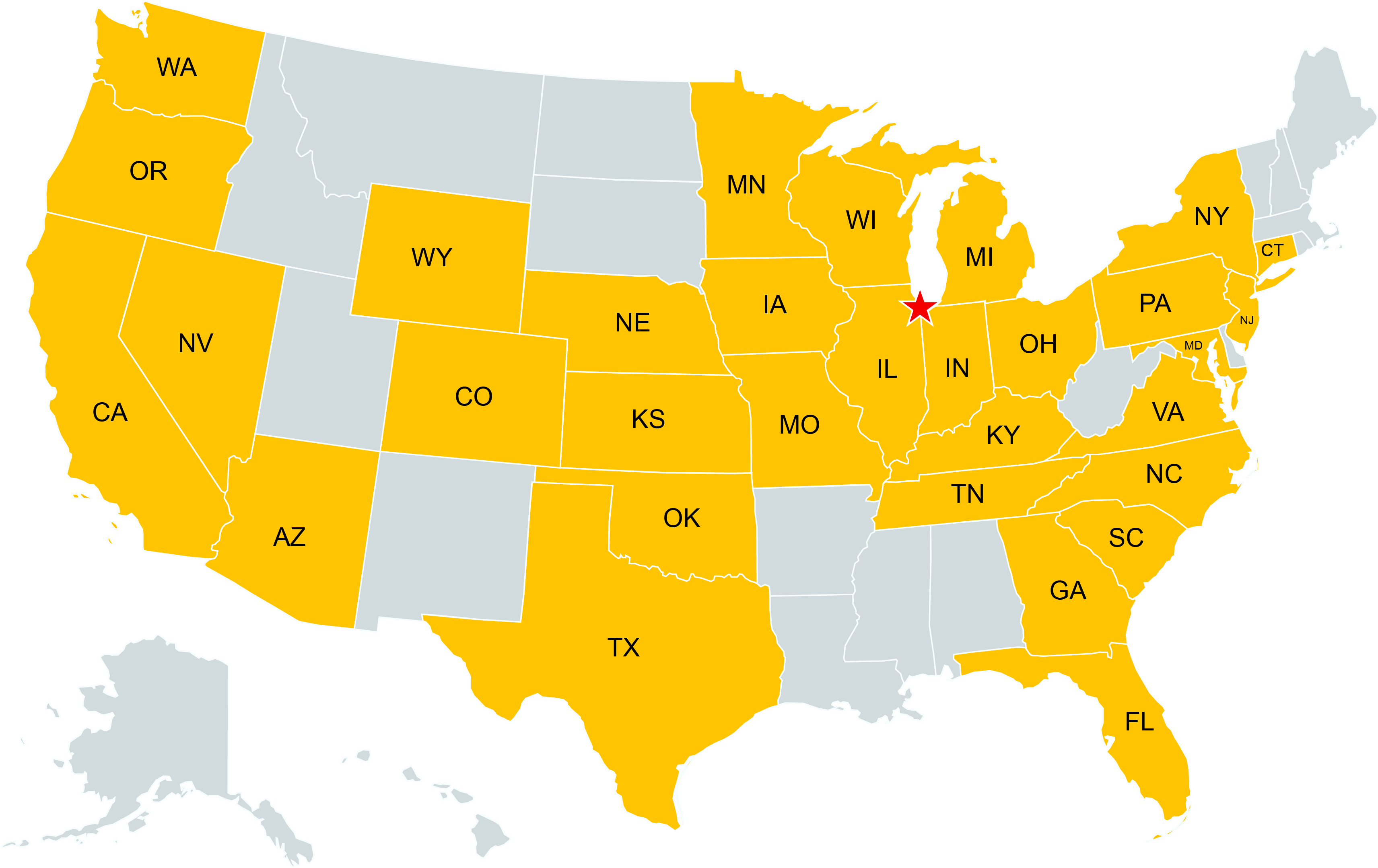

Where We Do Business