Insurance & Protection Planning

Protecting your wealth starts with protecting your life, income, health, and long-term future.

Our insurance and risk management strategies are built to give you and your family clarity, security, and confidence — backed by best practices, modern tools, and a philosophy focused on aligning everything with your bigger financial picture.

There is no perfect product.

But there is perfect planning: thoughtful, personalized protection designed around where you are now, and more importantly, where you want to be in the future- for yourself and for your family or business.

Our Approach to Risk Management

We take a comprehensive, planning-first approach to identifying risks that could disrupt your financial future — and then design protection strategies that support your long-term goals.

How we help:

We evaluate your life, income, family, business, and retirement risks.

We integrate the relevant insurance strategies into your financial plan cohesively.

We eliminate overlap, reduce gaps, and simplify your protection framework.

We coordinate everything with your tax planning strategy, investment strategy, retirement, and estate plan.

We proactively adjust your coverage as life evolves.

No pressure. No sales scripts. Just smart planning, objective guidance, and a long-term partnership.

The team at Sunny Financial Strategies, LLC are trained professionals who can help you identify your financial needs and then determine which financial and insurance products can best help you meet your objectives. Some of the products we often use to serve the needs of our clients include:

Life Insurance

1Many people think that life insurance is only for people with families. While it’s true that life insurance can help provide for the needs of dependents, life insurance also can be an important part of a well-thought-out estate, business succession, or charitable giving plan. And permanent life insurance offers many living benefits as well, such as tax-deferred cash value accumulation and tax-free withdrawals or loans.

For all of these reasons, Life Insurance is more than just protection — it’s a strategic tool for building, preserving, and transferring wealth.

Each type serves a different purpose, and we help you select the structure that aligns with your needs.

1Loans against your policy accrue interest and decrease the death benefit and available cash surrender value by the amount of the outstanding loan and interest. Accessing cash value will reduce the available cash surrender value and death benefit.

Term Life

Term life policies provide cost-efficient protection for a defined period—such as 10 years, 15 years, or 20 years.

Used for income replacement, mortgage protection, and covering temporary risks. Ideal for families with dependents, homeowners with a mortgage, and professionals looking for coverage outside of their employer benefits that they own and have more control of.

Term premiums are generally less expensive than permanent life insurance premiums, but once the term of the policy is complete, coverage terminates. There is no accumulation of cash value.

Why clients choose it:

Effective coverage during high-responsibility years

Ideal for families, new homeowners, and income replacement

Clean, simple structure with strong protection

Key Riders to Enhance Your Term Policy:

Conversion Privilege — Potentially convert your term policy to permanent coverage without medical underwriting for a defined window. This protects insurability and allows long-term planning even if health changes.

1Disability Waiver of Premium Rider — If you become disabled, your premiums can be waived, keeping coverage intact during difficult periods.

2Terminal Illness / Living Benefits Rider — Access a portion of the death benefit early if diagnosed with a qualifying terminal illness.

Ideal For:

Clients who want strong coverage now, with the future option to build long-term cash value or permanent protection.

1If this rider is purchased, New York Life will waive policy premiums should the insured become totally disabled, as explained in the policy. (Please note: Adding a disability waiver of premium rider to your policy involves an additional charge). This rider is available to insureds ages 0 through 59. In Maryland and Montana, this rider is not available until the insured has reached his or her fifth birthday. The benefits of this rider depend in part on when the disability occurs in relation to age 60.

2If you are diagnosed with a terminal illness and have a life expectancy of 12 months or less, the living benefits rider allows access to a portion of your policy’s eligible death benefit during your lifetime. It helps pay for critical medical treatments, and can be used to cover living expenses for your caregivers. This rider can be added to your policy at any time. Various states have established different life expectancy periods once a terminal illness is diagnosed. There are maximum benefit levels set for this rider. A charge is applied when the rider is exercised. Your agent can provide more specific information. Receipt of an accelerated death benefit may affect eligibility for public assistance programs and may be taxable. You should consult your tax advisor regarding your circumstances.

Whole Life

Whole life insurance is also known as permanent insurance. It has guaranteed premiums, guaranteed death benefit, and guaranteed cash value growth- as long as premiums (which are a set amount per period) are paid. Whole life policies accumulate cash value tax deferred.

Why clients choose Whole Life:

Lifetime coverage

Predictable, stable premiums

Cash value grows tax-deferred

Supports wealth-building, business planning, and legacy goals

1Available Riders for Whole Life:

Chronic Care / Chronic Illness Rider — Access part of the death benefit for qualifying chronic illness, helping cover care expenses.

Disability Waiver of Premium Rider — Premiums are waived after qualifying disability, ensuring the policy continues to grow.

Terminal Illness / Living Benefits Rider — Receive accelerated benefits in the event of a terminal illness.

Ideal For:

Professionals and business owners looking for long-term stability, tax-advantaged growth, and generational planning.

1Protects policy owners from the financial hardships of chronic care by providing tax-free access to a portion of their base policy benefits (death benefit) should they become chronically ill. This rider is available on most whole life and custom whole life policies (for an additional cost), and must be elected when the policy is purchased. This is a life insurance rider providing for an accelerated payment of the base policy face amount in the event that you are certified chronically ill as described in the policy. Receipt of accelerated death benefits may affect eligibility for public assistance programs and may have income tax consequences. You should consult your tax advisor regarding your circumstances. The Chronic Care Rider is not available in California.

Variable Universal Life (VUL)

Variable Universal Life Insurance combines the premium and death benefit flexibility of a universal life policy with investment opportunities. You may allocate your premium among a variety of professionally managed investment divisions plus a fixed account. Of course, with investment opportunities comes risk along with the potential for reward.

Why clients choose VUL:

Flexible premiums and death benefit

Potential for long-term cash value growth through investment subaccounts

Strong option for long-term accumulation and advanced planning

Tax advantaged savings, outside of traditional retirement accounts and rules

Key Riders for VUL:

Disability Waiver of Premium Rider — Protects your policy funding if you become disabled.

Terminal Illness / Living Benefits Rider — Access part of the death benefit in qualifying situations.

Guaranteed Minimum Accumulation Rider to align with risk tolerance and long-term goals.

Note: Riders vary by policy; suitability depends on risk tolerance and the need for long-term investment potential.

These products are offered by prospectus through NYLIFE Securities LLC. (member FINRA/SIPC), and a Licensed Insurance Agency.

Variable Universal Life is a type of permanent insurance that provides a death benefit in exchange for flexible premiums. The policy’s cash value will fluctuate, including investment gains and losses. Mortality and expense risk charges, cost of insurance charges, per thousand face amount charges, monthly contract charges, underlying fund charges, and any applicable surrender charges apply. Riders are available with purchase of a policy. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The underlying fund prospectuses contain this and other information. Please read the prospectuses carefully before investing. Issued by New York Life Insurance and Annuity Corporation (A Delaware Corporation), and distributed by NYLIFE Distributors LLC, Member FINRA/SIPC. Securities offered by properly licensed registered representatives through NYLIFE Securities LLC (Member FINRA/SIPC), A Licensed Insurance Agency. The Guaranteed Minimum Accumulation Benefit (GMAB) rider guarantees that at the end of the 12th policy year, the policy value in the eligible Investment Divisions of the base policy will not be less than the value of the GMAB account minus any unpaid loans and accrued loan interest. The GMAB account credits 2% on an annualized basis before fees and charges. The GMAB rider may be purchased for an annual fee. At the end of the 12th policy year, if your investment performance is less than the 2% crediting rate (compounded annually and gross of fees), then your policy will automatically be increased to reflect the adjusted GMAB account value.

Universal Life

Universal Life insurance is designed to offer customizable death benefit protection with non-guaranteed planned premiums and a non-guaranteed death benefit. Depending on the product selected and the amount of premium you pay, Universal Life insurance can allow you to keep your coverage as long as you need: to age 80, 90, 100 or longer.

Because of the policy’s flexible and non-guaranteed nature, it is important to fund your policy properly and actively manage your policy to reflect changes in interest crediting rates and policy charges over the duration of your policy. This policy will terminate if at any time the cash surrender value is insufficient to pay the monthly deductions. This can happen due to insufficient premium payments, if loans or withdrawals are made, or if current interest rates or charges fluctuate.

Why clients choose Universal Life:

Flexible funding: adjust premiums as income or needs change

Adjustable death benefit for evolving planning goals

Interest-credited cash value for long-term stability

Can support advanced planning (business, estate, policy layering)

Key Riders Available on Universal Life:

Disability Waiver of Monthly Deductions — Helps keep the policy active during qualifying disability

Terminal Illness / Living Benefits Rider — Access a portion of the death benefit early if diagnosed with a qualifying terminal illness

Chronic Care / Chronic Illness Rider — Access part of the death benefit for qualifying chronic illness, helping cover care expenses.

(Riders vary by product structure; some UL products may include additional options depending on the design)

Ideal For:

Clients seeking permanent coverage with flexibility and adaptability — especially helpful for business owners, families with changing needs, and long-term strategic planning.

Survivorship Life

Survivorship (Second-to-Die) Life insurance—available as whole life, universal life, or variable universal life —covers two people and provides payment of the proceeds when the second insured individual dies. Survivorship Life insurance is often used to help meet estate planning or business continuation goals.

Why clients choose Survivorship Life:

Ideal for estate planning and tax-efficient wealth transfer

Often more cost-effective than two separate policies

Useful for trusts, charitable gifting, business succession, and special needs planning

Helps ensure long-term protection for families and future generations

Ideal For:

Couples and families with significant legacy goals, estate tax considerations, trust planning needs, or long-term wealth transfer priorities.

Income Protection & Long-Term Care Planning

Disability Income Insurance

Your income is the engine that drives your entire financial life. If your family’s main provider is no longer able to work due to illness or injury, disability insurance protects your income so that your family still has a source of stability and helps ensure that your plan stays intact.

We can help you protect your current lifestyle and long-term goals. In addition to medical expenses, income is usually reduced or even terminated at the onset of an illness or injury. As the main provider for your family, you should strongly consider disability insurance if your spouse does not believe he or she could maintain financial stability with only one income.

Why clients choose this protection:

Replaces income during qualifying disability

Protects your savings, retirement contributions, and lifestyle

Fills gaps left by employer DI plans (often minimal)

Critical for high-income professionals and business owners

We evaluate:

Own-occupation definitions

Benefit amounts & benefit periods

Elimination periods

Riders such as residual/partial disability, cost-of-living, catastrophic benefits

Our goal is to help your income remain protected so your goals can continue uninterrupted.

Health & Medicare Coverage Guidance

Your health coverage is a cornerstone of financial stability. Whether you’re changing jobs, self-employed, approaching retirement, or evaluating Medicare options, we help you understand the costs, coverage levels, and timing that work best for your situation.

Health Insurance

We help you evaluate and compare your options to avoid costly gaps.

We guide you through:

Marketplace / ACA plans

Private health insurance

COBRA elections and timing

High-deductible plans and HSA optimization

Family and dependent coverage needs

Out-of-pocket cost planning

Our goal is to help you choose coverage that protects your financial plan — without unnecessary expenses.

Medicare

Medicare is complex. Choosing incorrectly can lead to penalties, higher costs, or limited doctor networks.

We simplify decisions surrounding:

Medicare Parts A & B

Medigap vs. Medicare Advantage

Prescription drug (Part D) plan considerations

Enrollment timing and penalty avoidance

Annual coverage reviews

Coordination with existing employer or retiree plans

You get clear, unbiased guidance so you can feel confident and prepared.

Disability and Extended Care

Long Term Care Insurance

To execute a sound retirement strategy, asset and income protection are a must. Designing a strategy that accounts for costs for extended periods of care and disability insurance can help create the necessary balance in a portfolio to ensure stability and protection of assets.

Disability Insurance

If your family’s main provider is no longer able to work due to illness or injury, disability insurance protects your income so that your family still has a source of stability. Our agents can help you protect your current lifestyle and long-term goals. In addition to medical expenses, income is usually reduced or even terminated at the onset of an illness or injury. As the main provider for your family, you should strongly consider disability insurance if your spouse does not believe he or she could maintain financial stability with only one income.

Individual disability insurance is available through one or more carries not affiliated with New York Life Insurance Company, depending on carrier authorization and product availability in your state or locality.

Annuities

An annuity is a unique financial vehicle designed to help you accumulate money for your retirement and/or turn a lump sum into a guaranteed stream of income payments. Deferred annuities offer the advantage of tax deferral and can be used to accumulate money for retirement. Income annuities are used to generate a stream of income payments that are guaranteed to last for as long as you need them to—even for the rest of your life.* Some of the different types of annuities are:

Fixed Deferred Annuities

With a fixed deferred annuity, the interest rate on your policy is guaranteed never to fall below a certain amount.* For many people, this provides a measure of security.

(A fixed deferred annuity is subject to a sales charge for early withdrawals, which may be subject to income tax. Withdrawals prior to age 59½ are subject to a 10% tax penalty.)

*Guarantees are dependent upon the claims-paying ability of the issuing insurer.

Lifetime Income Annuities

A lifetime income annuity is an annuity in which income payments begin one period after the annuity is purchased. It is designed to provide you with predictable income monthly, quarterly, semiannually, or annually, no matter how long you live, and regardless of how the financial markets perform.

All guarantees associated with annuity contracts are based on the claims-paying ability of the issuing insurance company. Withdrawals may be subject to regular income tax, and if made prior to age 59½, may be subject to a 10% IRS penalty. In addition, surrender charges may apply.

Variable Deferred Annuities

A variable deferred annuity offers the advantage of tax deferral and can be used to accumulate money for retirement. The policy's accumulated value—and sometimes the amount of monthly annuity benefit payments—fluctuates with the performance of your variable investment account options. There are fees, expenses, and risks associated with the contract. Please be aware that assets allocated to the investment divisions are subject to market risks and will fluctuate in value.

Offered through NYLIFE Securities LLC (member FINRA/SIPC), and a Licensed Insurance Agency.

Investors are asked to consider the investment objectives, risks, charges, and expenses of the investment carefully before investing. Both the product prospectus and the underlying fund prospectuses contain this and other information about the product and underlying investment options and can be obtained from your Registered Representative. Please read the prospectuses carefully before investing.

Business Owner Protection Planning

As a business owner, your personal financial future is deeply connected to the stability and continuity of your company. We help you design protection strategies that safeguard your income, ownership, key people, and long-term business value.

Each of the following solutions is tailored to the size, structure, and goals of your business — and integrated seamlessly into your overall financial plan.

Why Business Owner Protection Matters

Without proper planning, a single unexpected event can impact:

Business valuation

Cash flow

Ownership control

Employee morale

Revenue

Your personal financial future

We help business owners reduce risk, preserve enterprise value, and protect what they’ve worked so hard to build.

Key Person Insurance

The success of many businesses depends on a few critical people — owners, executives, or top performers.

If one of them becomes disabled or passes away, it can create financial strain, disrupt operations, and jeopardize the company’s stability.

Key Person coverage provides:

Capital to offset lost revenue

Funds to hire or train replacement talent

Liquidity to maintain operations during transition

Confidence to lenders, partners, and clients

Strengthened succession planning

Best for:

Businesses with partners, top salespeople, specialists, or irreplaceable talent.

Buy-Sell Agreement Funding

A Buy-Sell Agreement only works if it is properly funded.

We help you ensure that ownership transitions are smooth, tax-efficient, and fully capitalized — whether triggered by death, disability, retirement, or voluntary sale.

Types of Buy-Sell structures:

Cross-purchase

Entity purchase (stock redemption)

Wait-and-see plans

One-way buy-sell for sole owners

Funding strategies we use:

Life insurance

Disability buy-out coverage

Hybrid structures for liquidity events

Why it matters:

Without proper funding, surviving owners may face forced sales, debt, legal disputes, or loss of business continuity.

Executive Benefits & Retention Strategies

Top talent is hard to find and even harder to keep — especially in competitive industries like healthcare, tech, engineering, consulting, and professional services.

We design executive benefit strategies that reward key employees, promote loyalty, and align compensation with long-term business goals.

Common solutions:

Supplemental Executive Retirement Plans (SERPs)

Executive bonus plans (162(b) plans)

Restricted executive benefit arrangements

Split-dollar life insurance arrangements

Deferred compensation structures

Golden handcuff retention plans

Benefits to the business:

Helps recruit and retain top performers

Incentivizes loyalty and long-term commitment

Provides structured retirement or supplemental income benefits

Creates tax-efficient compensation models

Benefits to the executive:

Additional retirement income

Personalized life insurance or protection benefits

Long-term wealth-building opportunities

Business Overhead Expense (BOE) Planning

If a business owner becomes disabled, fixed expenses don’t stop. BOE coverage helps ensure the business can stay open while the owner recovers.

BOE helps cover:

Rent or mortgage

Utilities

Staff salaries

Insurance premiums

Office expenses and loans

Why it matters:

Keeps the business financially stable and preserves enterprise value during periods of owner disability.

Loan & Debt Protection Strategies

Banks and lenders often require coverage on business owners — but even when they don’t, loan protection is a smart risk-management tool.

Loan coverage helps:

Repay business loans if an owner passes away or becomes disabled

Protect co-signers and partners

Maintain business credit strength

Prevent forced liquidation of assets

Business Succession & Continuity Planning

A business transition is one of the most financially significant events in an owner’s life. We help you prepare for planned and unplanned exits.

We guide you through:

Succession plan structure

Ownership transfer strategy

Tax-efficient exit planning

Retirement income planning for the selling owner

Business valuation coordination

Funding strategies for internal or external buyers

Whether your plan includes family succession, partner takeover, or future sale, we help ensure your exit is financially secure and well-executed.

Owner & Shareholder Income Protection

Your personal income often depends on business revenue. Disability or serious illness can disrupt both your lifestyle and the stability of your company.

We design:

Owner disability income replacement

Disability buy-out strategies

Business continuation income protection

Layered coverage for high-income earners

This ensures both your personal plan and your business remain stable.

Products available through one or more carriers not affiliated with New York Life Insurance Company, dependent on carrier authorization and product availability in your state or locality.

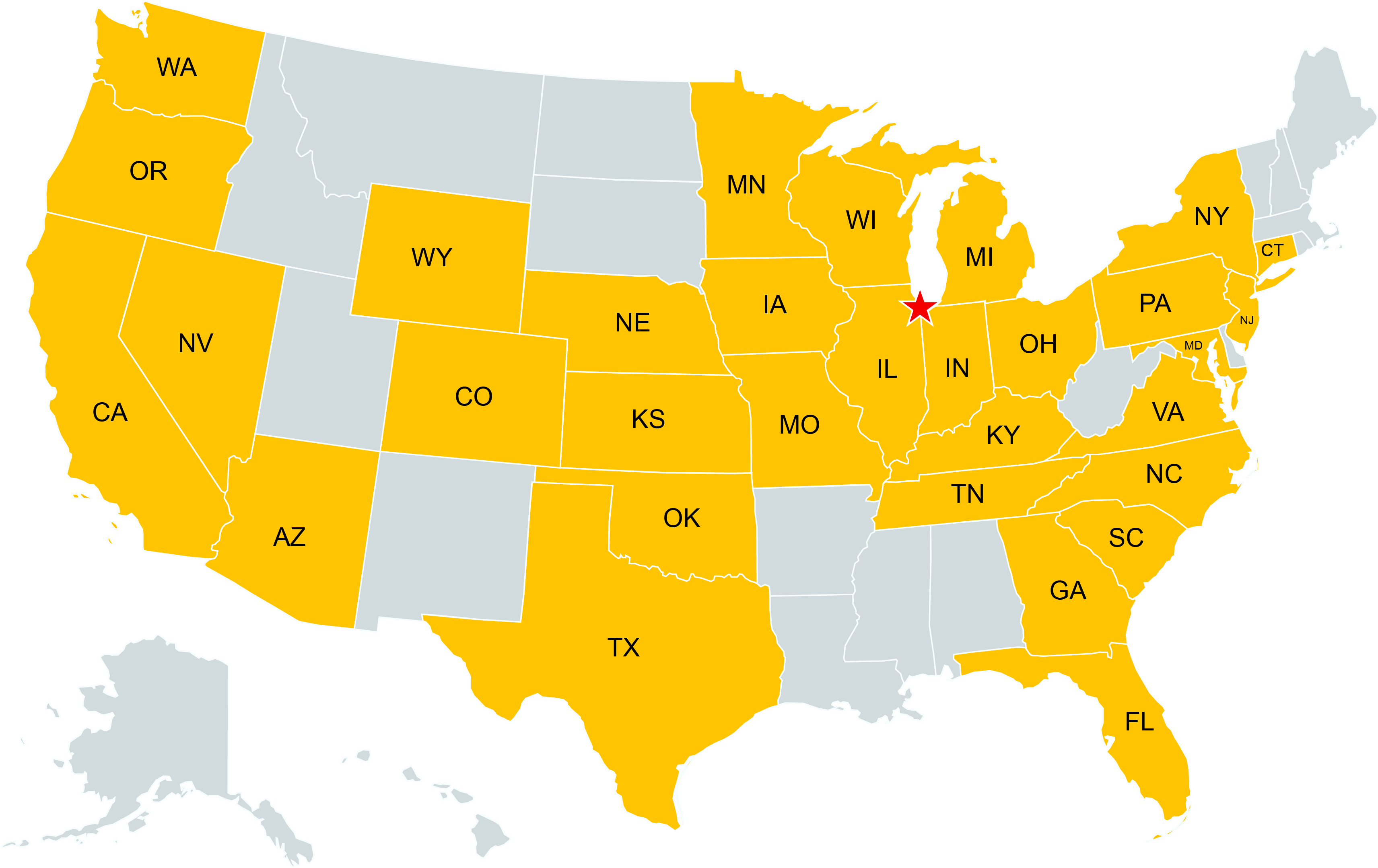

Where We Do Business